With all the good weather we have had in the past few weeks, could rising interest rates be some extra sunshine on the horizon for Trustees and Sponsors of Defined Benefit (“DB”) pension schemes?

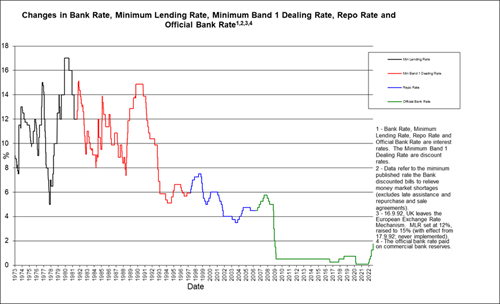

Recent months have seen climbing interest rates and long-term government bond yields. This is coupled with the Bank of England recently increasing the base rate to 1.75% from 1.25%, the largest increase in nearly 30 years. The chart below, from the Bank of England, shows changes in interest rates over the past 50 years.

But what does this mean for DB pension schemes?

All else being equal, a rise in the interest rates will lead to a fall in the value of DB liabilities. This means schemes are likely to have seen a gradual improvement in their funding level over the last 18 months with a lot of schemes catching up on covid losses from 2020 and even surpassing pre-covid positions.

In particular, schemes with lower levels of hedging, who may have previously been at greater risk during periods of falling interest rates, could be seeing material gains in their funding positions. On the other side of the coin, schemes with higher levels of hedging and Leveraged Liability Driven Investments (“LLDI”) may be facing the difficult challenge of potentially missing out on these sizeable gains and also liquidity issues due to significant collateral calls from LLDI managers.

It is not only the scheme funding basis that will be improving but rising interest rates can also change the landscape for pension schemes in general and what was previously unthinkable before may now be in sight – that’s right – ‘buy-out’. With buy-out funding positions also improving, in line with recent guidance from The Pensions Regulator, trustees and employers should carefully consider their long-term objectives for their scheme. Can buy-out now be targeted sooner? Should changes be made to the scheme’s current funding path? Such considerations will soon become mandatory under prospective requirements for defined benefit (DB) schemes to produce a long-term funding and investment strategy statement.

There are lots of points to consider but the main take away from the rising interest rates is that trustees and employers should remain alert to positions changing quickly and consider ‘locking in’ some of the recent gains. For example, this may mean taking investment risk off the table and increasing hedging. Schemes who have access to state-of-the-art technology and immediate visibility of daily funding levels will be in a position to take advantage of any movements and gains. Don’t miss the boat! These considerations are echoed by the Regulator who said it is a good time for pension schemes to seek future protections.

Though, as always, the path is not all sunshine and rainbows and is slightly clouded by rising long-term inflation rates which will work in the opposite direction and push a schemes funding level down. Thankfully, this can be mitigated by hedging and inflation capping of member’s benefits. More information on high inflation levels is in our blog “What does rising inflation mean for defined benefit pension schemes?”, written by Angela Burns.