Many aspects of 2020 have highlighted how things that historically had been taken for granted needed to be questioned and new thinking encouraged. Who would have thought at the start of 2020 we’d have a nation living its business life on Zoom or Teams? But people have adapted to the new norm.

In terms of LGPS, and particularly LGPS exits, the movements shown in the chart below have served to highlight just how flawed a process calculating exits based upon gilt yields really is; well for everyone except the Funds that is!!

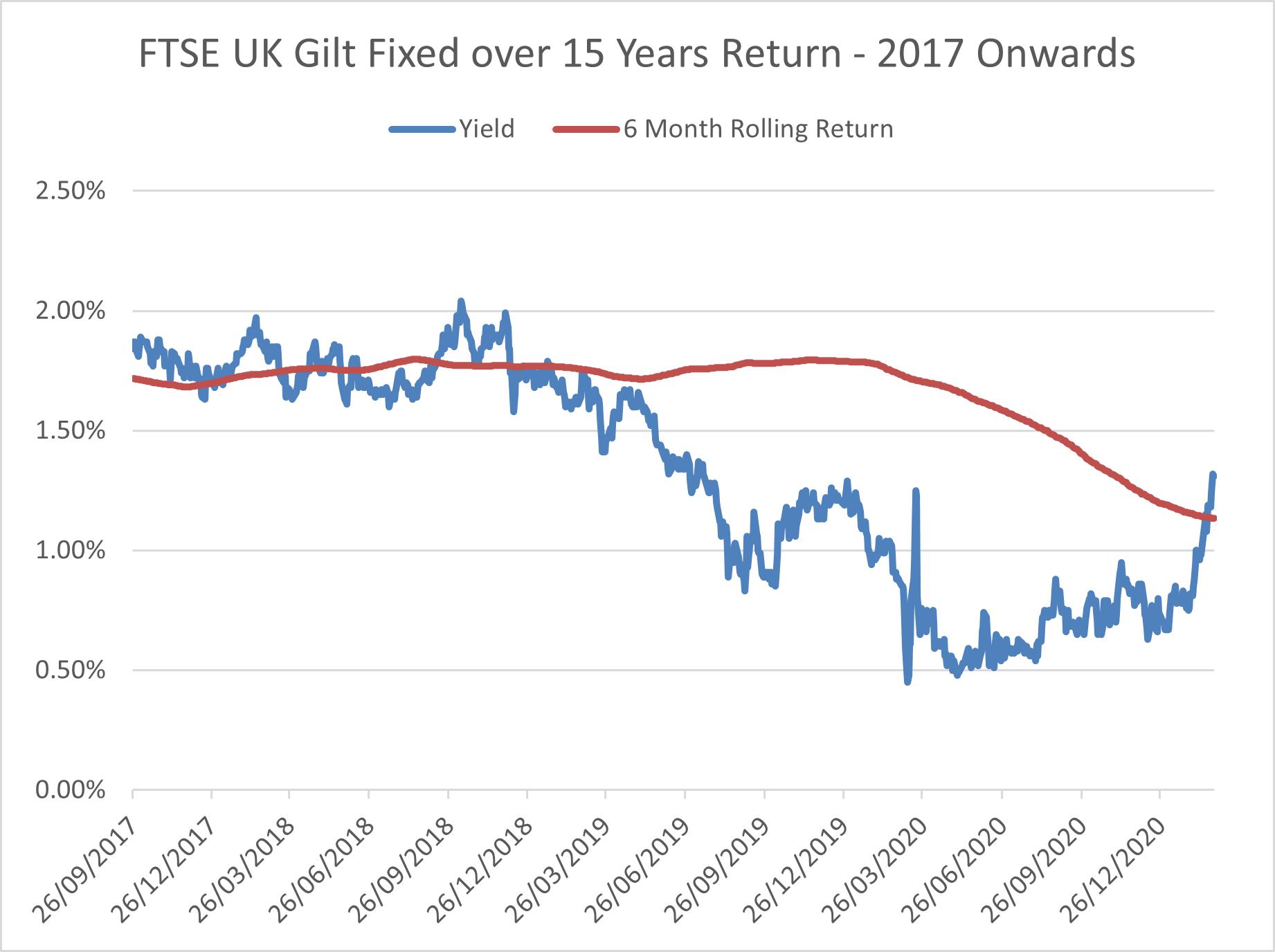

The table below shows 15-year UK gilt returns since 2017.

Until 2019, we saw yields bouncing along at somewhere between 1.5% and 2.0%, so exit debts at that point would have been fairly consistent and would have been pretty close to the 6-month rolling average. However, from mid-2019, yields went on a downward trend, which continued through much of 2020 with only a more recent upturn.

It’s an understatement to say that yields have been volatile in 2020, fluctuating from a high of about 1.3% to a low of close to 0.4%. Indeed, the graph shows that over a one-month period, yields fell from 0.85% to 0.4% before rising to 1.2% and then falling back to just over 0.6%. I re-iterate that this was over a one-month period!!! All very interesting I hear you cry but what does this mean for me?

Well, LGPS exit liabilities are calculated based primarily upon gilt yields (and inflation) with the ultimate deficit also dependent on asset values.

Taking a high-level example, if you had cessation liabilities of £1.6m on the 31 January 2020 these could have increased to about £1.8m at the end of February, fallen to about £1.1m at the end of February, before increasing to about £1.7m by the end of March. So, about a £600k swing or approximately 45% over a matter of a few weeks. We’ve then had a material improvement in yields in 2021, up to about 1.3% currently.

If we then factor in changes in asset values, cessation debt swings could be absolutely enormous purely as a result of timing.

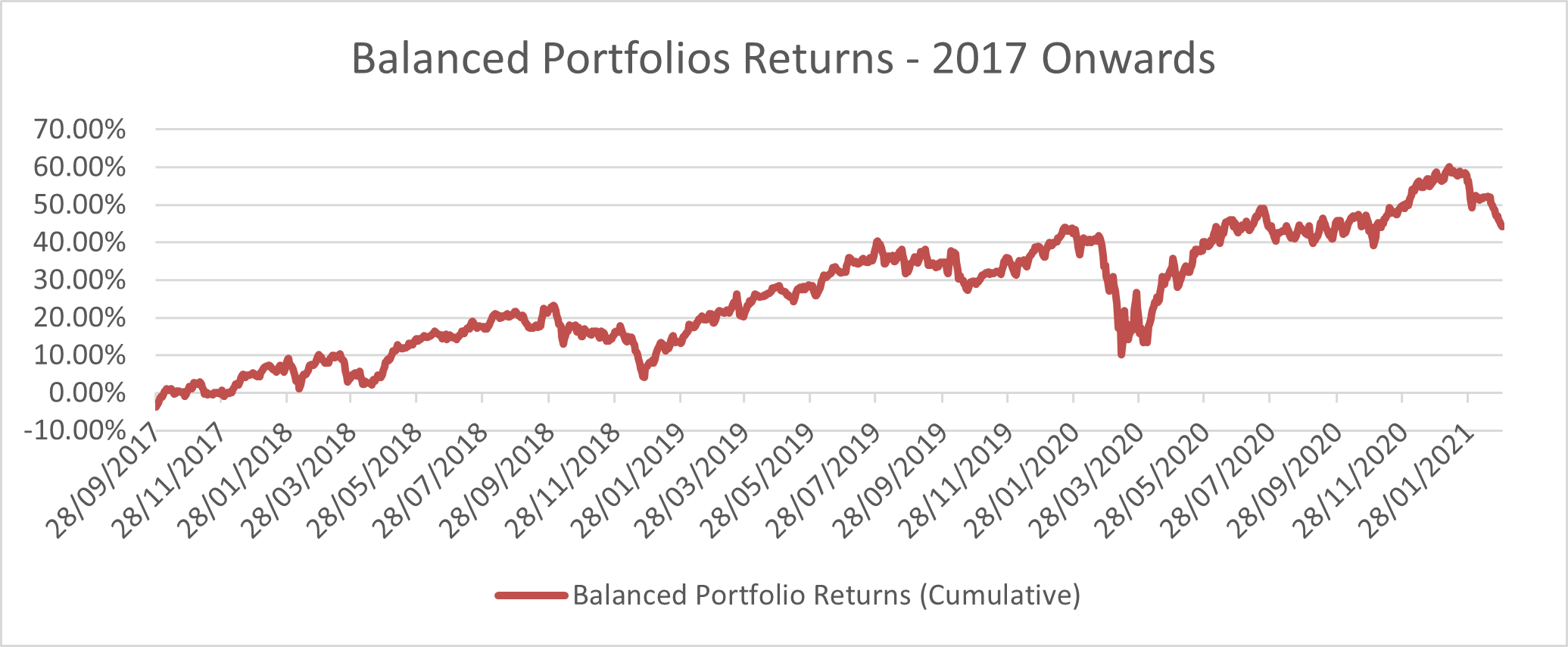

Taking a balanced portfolio return similar to LGPS and used as a proxy over the same period, you can see that organisations seeking to exit in 2020, or even worse being forced to exit, will have fared very badly in terms of their cessation debt figure through low gilt yields and suppressed investment values.

So, if we started with £1m of assets and £1.6m of cessation liabilities resulting in a deficit of £600,000, this could have increased to close to around £1m by the end of March 2020. Interestingly, the deficit could currently be much smaller than the position at the start of 2020.

An important point to note here is that gilt yields do not reflect the actual cost of providing the benefits, but purely a theoretical cost of ‘securing’ them at that point. However, the benefits in the Funds are not secured on exit but remain invested, usually in the main fund investment strategy, which will not reflect gilts. Funds, therefore, benefit from the gilt exit payment through higher assets and continue to invest these to achieve a higher return [See Bulletin 35 - Charities cross subsidising public bodies]. This discounts their future costs at the expense of the exiting employer.

I can understand that there needs to be some protection of other participants in the Fund when an employer leaves, but the current system is wholly inequitable and bordering on profiteering. I can only hope that Funds apply the new deferred debt flexibilities brought in to LGPS Regulations from September 2020 in a fair and transparent way. This will allow exiting employers some realistic exit terms which reflect a more balanced position.