Overview

The Pensions Regulator (TPR) has launched a discussion on its 15-year Corporate Strategy to protect savers[1].

Reflecting the changing nature of workplace pensions, the Corporate Strategy, which should have been issued in the Spring but was delayed because of COVID-19, outlines a shift in focus, over time, from defined benefit (DB) to defined contribution (DC) pensions, at least in the private sector. The strategy also builds on TPR’s transformation to be a ‘clear, quick and tough regulator’.

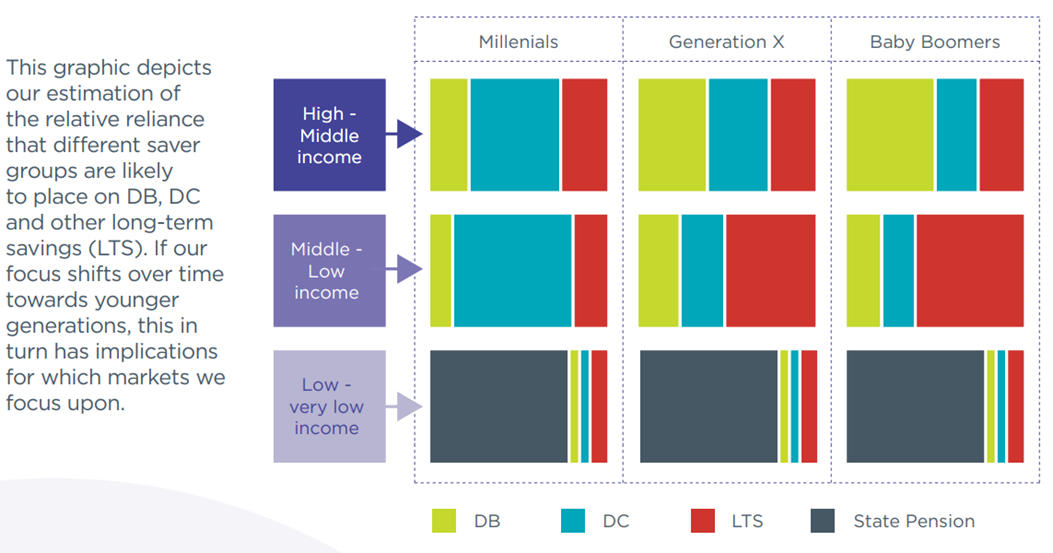

The strategy analyses different groups of savers by generation – Baby Boomers (born between 1946 and 1964), Generation X (1965 and 1984) and Millennials (1985 and 2004) – recognising that each group faces different life circumstances and risks in relation to their pensions (see extract below).

For younger savers automatically enrolled into DC pensions, TPR observes that ‘investment performance’, ‘value for money’ and ‘at-retirement decision-making’ will play a much greater role in retirement outcomes.

From this analysis five strategic priorities emerge:

- Security - protecting the money that savers invest in pensions. Maintaining focus on the promises that are made to savers in DB schemes and on protecting their pensions from scammers; over the fifteen-year horizon of the strategy, as assets in DC schemes grow, there will be a shift in primary focus to the security and value that these schemes provide savers.

- Value for money - savers’ money must be well-invested, costs and charges must be reasonable; and good quality, efficient services and administration must be driven by robust data.

- Scrutiny of decision making - monitoring those who make decisions that impact savers’ outcomes, closely scrutinising any decisions that pose a heightened risk to the quality of these outcomes.

- Embracing innovation - encouraging innovation and good practice, collaborating with the market to enhance security, efficiency, transparency, simplicity, and choice.

- Bold and innovative regulation - transforming the way TPR regulates to put the saver at the heart of its work, driving participation in pensions saving and enhancing and protecting savers’ outcomes; maintaining a sharp focus on bold and innovative regulation, anticipating and preventing issues before they materialise.

The strategy has been published in the form of a discussion paper, with four issues highlighted (see the questions below), and meetings with key stakeholders are planned. The final strategy will be published in the new year and the strategic priorities will form a core part of TPR’s annual three-year corporate planning going forward.

|

Q1 |

Do you think our approach to thinking about savers has identified the most significant current and future challenges for each cohort? |

|

Q2 |

To what extent should we differentiate our approach to regulation for these different saver groups? At what pace would you expect to see this happen? |

|

Q3 |

Do you think the key trends we have identified adequately capture the most likely system-level changes pensions will experience over the next 15 years? Are there other system level changes you believe we need to consider? |

|

Q4 |

Do our strategic priorities provide the coverage, focus and flexibility we need to achieve our ambitions for savers over the next 15 years? |

What can we learn from this paper?

Taking each of the above priorities in turn, key points from the discussion paper are:

- There is still much to do for members of DB schemes (including impact of COVID-19, new Funding Code and combatting pension scams) but, as the shift to DC continues, TPR’s focus will move from a scheme-based view to one focussed on the saver.

- As we become a nation of ‘DC dependents’ (individuals who have only ever been in DC schemes), TPR’s focus will be on making sure that those schemes are well run and provide value for money.

- TPR expects dashboards and fintech to increase transparency and reduce the cost and effort of making decisions. A shift in the trustee model is predicated, with fewer, more professionalised trustees.

- In future, savers will have longer and more varied working lives and this has an impact on how and when they save for retirement and the products, guidance and advice they will need. Market innovations will require improved data quality but advances in technology should improve both the quality and security of data.

- TPR expects to be regulating fewer but larger schemes of all types as the market consolidates: for occupational DC this could be around 50% fewer schemes and for DB around a third fewer. Also, in 15 years, the UK will be halfway towards its legally binding net zero emissions target and this means all pension schemes’ investment decisions will need to take account of climate risk.

Of course, the old adage ‘we live in interesting times’ has never been more apt and so it is important to note that the strategy paper is specifically stated to be a ‘living document’.