Update on SPPA Consultation

Our last bulletin 58 explained the consultation process being run by the SPPA, proposing to make exit credits from LGPS funds in Scotland discretionary rather than mandatory from 29 June 2024 onwards. This would bring the Scottish regulations in line with England and Wales. Implementation has now been delayed on account of SPPA receiving a higher number of responses to the consultation than expected.

The changes will most likely still happen, but for now funds in Scotland still have to pay an exit credit if there is a surplus on cessation of a participating employer.

We partnered with Burges Salmon to hold a webinar on 23 July 2024 giving details on how the discretion might be applied by funds and to discuss practical steps for LGPS employers participating.

This bulletin gives more detail on what was discussed during the webinar regarding LGPS employers.

How will the discretion be applied?

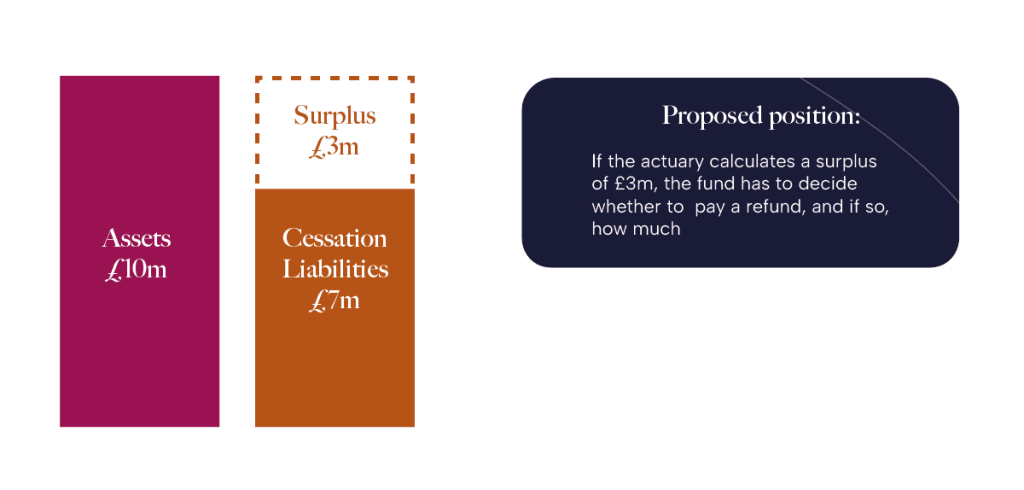

Currently any surplus calculated on a cessation basis is payable as an exit credit to the employer. In this example, the £3m cessation surplus is payable to the employer if they were to exit from their fund.

Under the new regulations the fund would have the right to decide whether a refund would be paid at all and if so, how much.

The draft regulations set out some considerations for funds when exercising their discretion, which broadly mirror the factors which funds in England and Wales must consider. These are:

- What is the extent of the surplus?

Funds may be more likely to pay an exit credit if the employer has a large surplus and has been in surplus for a long time, as the surplus is then permanent rather than a temporary feature which could be the case if employers just tip into surplus from time to time. - What was the level of employer contributions?

Funds should consider the proportion of the surplus which has arisen from the value of the employers’ contributions and may be minded to cap an exit credit at the level of contributions paid in by the employer. - Representations by the employer

If an employer makes a representation, it has to be considered by the fund. An employer that has borne the funding risk and paid significant deficit contributions might make a representation that as it was exposed to the downside risk, it should be able to access a surplus emerging from upside risk. - Any other relevant factors?

An administering authority should consider relevant factors and disregard irrelevant factors when making a decision. Ultimately the decision needs to be reasonable and defensible. This will include the level of contributions and the level of surplus, but it might also consider netting off future running costs for the scheme linked to the liability of the withdrawing employer, which will need to be administered and paid for over time.

An irrelevant factor could be where an employer is in dispute with the administrative authority completely outside of the pension context, such as a planning dispute. That would be a factor not relevant to this specific decision and therefore disregarded.

What can we learn from England and Wales?

As the proposed regulation change creates the same environment as England and Wales there is the opportunity to learn from how funds have dealt with the issue there.

Some noticeable adjustments that have been made in England and Wales have been capping the level of any exit credit at the level of contributions the employer has paid into the fund and deducting the expected future administration and running costs from the refund payment, reducing the value of credit payments.

Emerging Trends: Hardening of Exit Bases

In England & Wales, and also in Scotland, we have already begun to see some funds hardening the exit basis in a range of different ways including the use of cessation corridors and risk-based calculations.

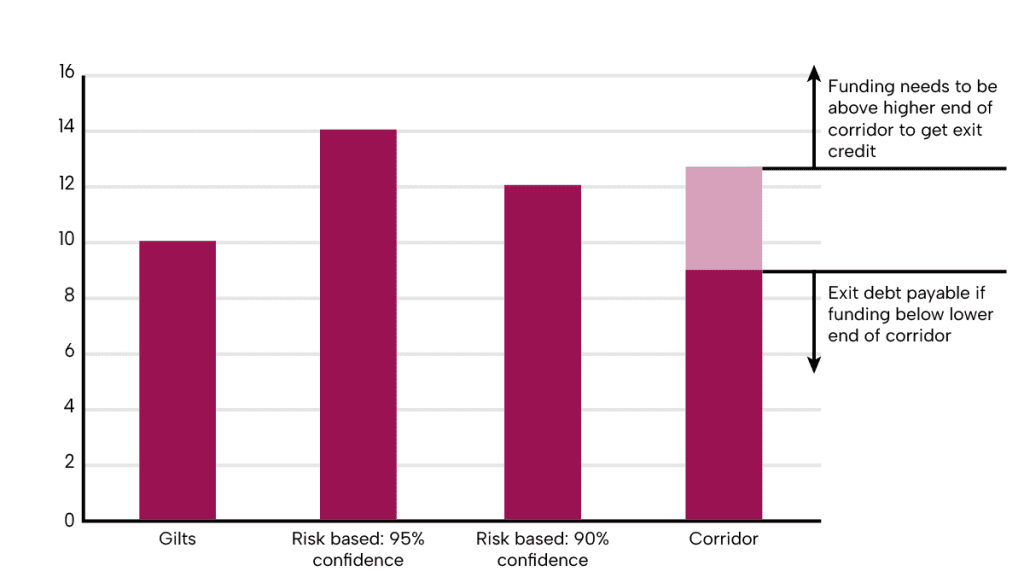

Historically cessation bases have been based on a gilts approach where the discount rate has been set in line with gilt yields. When gilt yields were low, this placed a high value on the liabilities, resulting in higher exit debts.

Over the last couple of years we have seen a sharp rise in interest rates, resulting in materially lower liabilities being calculated on a gilts basis, reducing the value of exit debts and in some cases resulting in an exit credit.

Funds have started to change their approach to calculating cessation bases to try and mitigate risk – the funds may be in surplus now, but this may not be the case in the future. Funds are trying to take account of this in their alternative approaches to calculating cessation positions.

Shift Towards Risk-Based Calculations

One approach we are seeing a shift towards is funds using risk-based calculations. Funds are trying to ascertain what level of funds they need to set aside today to give a reasonable chance of sufficient funds being in place for the coming years, rather than just considering the funding position at the cessation debt.

Generally speaking, this results in a higher liability than a gilts based approach, meaning higher exit debts/lower exit credits, as illustrated, with liabilities of between £12-£14m compared to £10m on a gilts basis.

The liabilities are also very sensitive to the probability of success that is used. Moving from 95% to 90% could take over 10% off the liabilities and vice versa. If the fund were 110% funded on the cessation basis using a 90% probability of success, it could wipe out an exit credit entirely by simply moving to a 95% probability of success.

Another approach we see being used is a “corridor approach” to cessations. If the funding level is in the corridor, i.e. higher than the lower end of the corridor and lower than the top end of the corridor, no debt will be paid, but equally no credit will be paid. You need to have a funding level in excess of the high end of the corridor before any exit credit would be paid.

In the example we are showing a low end of approx. £9m and a higher end of just over £12m. To receive any exit credit, you would need assets in excess of £12m. This approach is good if you are underfunded as it could result in no exit debt or a lower exit debt being payable. But it is harder to get an exit credit.

Different funds use different actuaries, and the cessation approaches and results are heavily reliant on this. Different actuaries will use different assumptions in the calculations, so for example a 95% probability of success in one fund may not give the same exit position as a 95% probability of success in another fund advised by a different actuary.

One point to note is that although the exit and cessation bases are hardening from a market conditions perspective, it’s still an attractive time to exit in terms of funding levels.

Funding levels have improved a lot more than even these hardening of the bases, the outcome of this in most cases is the surplus is smaller than it was before, but not necessarily pushing you back into deficit on one of these cessation bases.

Take a look at these case studies that bring to life how funds might administer their new discretions.

- The Outsourcer – £10m assets: £7m cessation liabilities | £3m surplus – Participating in the LGPS via an outsourcing contract with pension costs are passed through the authority.

- The Charity – £10m assets: £7m cessation liabilities | £3m surplus – Long standing participant who has paid substantial deficit contributions.

- The Guarantee – £10m assets: £8m cessation basis | £2m surplus £6m ongoing basis | £4m surplus – employer has a guarantee from the Council. Employer only needs to fund the liabilities on an ongoing basis rather than a cessation basis and is in surplus on both measures on an exit.

Conclusion

For now funds in Scotland have to pay exit credits if there is a surplus on cessation, so employers can continue to plan for exits on the basis of receiving an exit credit. But the new regulations are likely to come into force in due course, at which points employers will need to understand how funds will exercise their discretion to pay an exit credit.

If you have any questions about the upcoming changes to exit credits in Scotland or need guidance on navigating the new discretionary framework, please don’t hesitate to reach out. We’re here to help you understand the implications and explore the best strategies for your specific situation.