Alistair Russell-Smith thoughts on the significance of 5 June 2025

5 June 2025 may go down as one of those seminal dates in the world of UK DB pensions, like the 17 May 1990 Barber window date and ‘A day’ on 6 April 2006. Why?

Pension Schemes Bill 2025 and the major changes for DB schemes

Firstly, the Pension Schemes Bill 2025 was released, introducing wide sweeping reforms across DC and DB pensions. From a DB perspective, it will permit surplus release from ongoing schemes and legislate for superfunds to encourage growth in that market. This should make a wider range of endgame options like run-on and superfunds genuinely viable for a broader range of DB schemes.

Secondly, on the same day the DWP confirmed that they will introduce legislation to allow retrospective actuarial confirmation that historic benefit changes met the “Reference Scheme Test,” thereby removing a significant risk that could have led to additional liabilities for many pension schemes off the back of the 2023 Virgin Media Court case.

Whilst these are welcome developments, which over time will give much needed clarity to pension scheme trustees and sponsors and market participants, it will be some years before we get through the required secondary legislation and consultation processes for the developments to become effective.

What Trustees and Sponsors should do now

In the meantime, we have pressing data projects and deadlines that DB schemes need to meet. So how should DB trustees and employers navigate these developments, set their strategy and prioritise work and projects?

Strategies need to reflect the objectives, priorities and circumstances of individual trustee boards and sponsors, but below is a suggested approach for schemes operating under business-as-usual, rather than those facing a corporate transaction or other significant event:

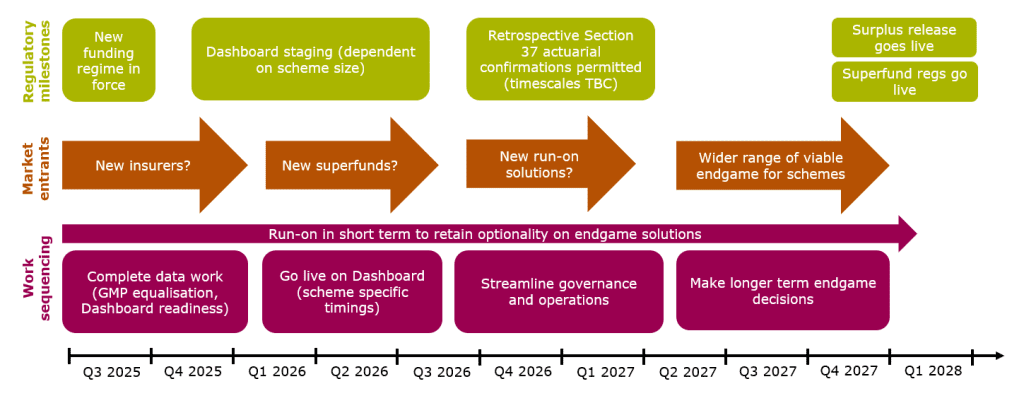

- Retain optionality on endgame solutions for now. These regulatory developments should lead to more participants in the insurer and superfund markets, and enable surplus release from ongoing schemes, meaning from 2028 onwards a full suite of viable, competitively priced endgame options should be available. For signing off a triennial valuation under the new funding regime, of course have a plan for reaching full funding on a low dependency basis (if you are not already there), but go no further than that for now.

- Prioritise completion of required data projects in the short term. Many schemes still need to finish GMP equalisation, and most need to connect to the Pensions Dashboards over the next year. With some administrators facing resource constraints, this has to be the short term priority. It ensures you comply with impending deadlines, and helps give you clean, complete data that has benefits for all the endgame options.

- Streamline the operations and governance of the scheme. Get the benefits fully coded and the calculations fully automated on the administration system, address retrospective actuarial confirmation of historic benefit changes if required, and consider leaner models like sole trustee and multi-trust solutions. This all reduces running costs, making run-on more viable and enabling quicker implementation of risk transfer end game solutions (either to insurers or superfunds).

- Make endgame decisions in 2027/28 when we should have more competitive insurance and superfund markets, and clarity on how ongoing surplus release can operate.

Looking ahead: Timeline and key milestones

What are the timescales for these regulatory developments and sequencing of work? Well we’re still waiting for details on some of this, although we know the government intends the surplus release and superfund regulations to go live in 2028, so working back from that, the plan looks like this:

Why 5 June 2025 marks a turning point

5 June 2025 could become a pivotal date in UK pensions history; the day superfunds and run-on became truly viable, and the headaches from the Virgin Media ruling disappeared!

While the recent reforms don’t require immediate action, they do expand the range of viable strategic options for many DB schemes. Trustees and sponsors should now take the opportunity to revisit their long-term strategy and assess how these developments might benefit their specific circumstances.

If you would like to discuss what these changes could mean for your scheme, please get in touch.