Don’t let data hold up your pension journey

A familiar frustration, the Summer holiday queue

Despite the stereotype of an amiably queueing British public, being stuck in line when your preferred outcome is at stake is nonetheless frustrating.

You might have failed to pick up on the confusing passport renewal rules while you have been measuring your hand luggage to avoid a fine for having the audacity to carry on a few extra centimetres of baggage.

Now you are caught in the passport application queue behind the rest of the desperate, summer-holiday bound. What if it doesn’t make it to you on time? A costly cancellation and rebook?

Not to mention the disappointment and wasted hours of research you spent getting the best deal in the first place. Now you might have to settle for the anticipation of allocation on arrival!

From holiday panic to pension risk: The analogy

Now think of a pension scheme, heading for buyout. This is a familiar risk in any DB pension risk transfer process. Timelines are set, costs approved, you might have already completed a buy-in and the final step is just around the corner. But what if your data and benefits are not up to scratch for the tip top transaction you have planned for? Now the insurer requires more money to account for the adjustments to align to the policy.

Now the administrator has popped you in the queue of other data projects and your agreed timelines are beginning to slide, along with your confidence in the quality of this transaction.

An irrevocable decision demands certainty

As a pension scheme trustee who undertakes a bulk annuity transaction with an insurer, you are making a forever, irrevocable transaction. One where, (after wind-up) the insurer has no recourse to the Trustees or Sponsor should issues arise.

The trustee must also, at the point of wind-up, confidently discharge their responsibilities knowing they have done their best to insure the right members with the right benefits.

Both points of view highlight the clear benefit of ensuring scheme data is in good quality before approaching the market to make that irreversible, lasting and absolute decision. A well-prepared DB pension risk transfer depends on accurate, complete data.

The hidden cost of poor data quality

Transacting with poor quality data leaves you exposed to material cost uncertainties. To execute the buy-in Trustees would have signed the insurer’s bulk annuity policy terms. This outlines the insurers expectations of any data and benefit cleansing requirements (to be completed by the Trustees after buy-in) and the consequences of any material changes as a result of the cleansing exercise.

The ‘true up’, or price of the adjustments needed to align the policy to the final, cleansed, data and benefits could be an unexpected and significant ask. Where will the extra funds come from? Will the Trustees need to ask the Sponsor for additional funding? Will any surplus initially expected to be distributed back to the sponsor and/or scheme members be depleted? All outcomes I am sure best avoided or at least mitigated as far as possible.

Why this matters more than ever

With many DB schemes in a well-funded position, this has accelerated the volume of DB pension risk transfer activity in recent years. We are seeing a greater number of schemes coming to market looking to complete full scheme buy-ins, then move to wind-up and buyout.

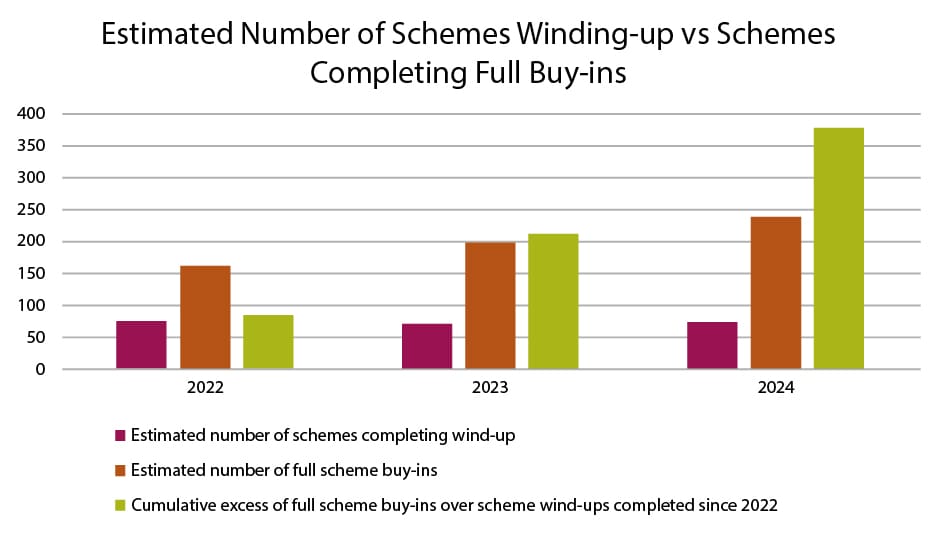

Over the last 3 years (2022 to 2024), we have seen c750 bulk annuity transactions completed covering some c£125bn of pension scheme liabilities. With the majority of these transactions being full scheme buy-ins, which will lead to wind-up and buyout in the vast majority of these cases. This represents c15% of the universe of private sector DB pension schemes (by number) and the trend appears to continue upwards fuelled by attractive market conditions and increased capacity from new entrants.

The current capacity crisis

To approach the market for a bulk annuity, transact, complete data cleansing requirements, complete a scheme wind-up and buyout all require substantial amounts of administration resource way beyond BAU administration tasks. These tasks are onerous for the scheme and insurer, therefore understanding the requirements and obligations to the insurer are vital.

Investigating the PPF Purple Book more closely to try and understand how many schemes are successfully completing wind-up each year, we can see that consistently, year on year, between 80 and 100 schemes have “disappeared” annually over the last 5 years from the Purple Book statistics.

However, there is no breakdown between schemes winding-up, schemes entering the PPF or schemes being merged into other schemes. That means we can confidently assume that well under 100 private sector DB schemes have actually achieved wind up in the UK each year on average over that 5 year period.

When we compare that to c750 schemes completing buy-ins in the last 3 years, with possibly 600+ of these being full scheme buy-ins, this means that the number of schemes heading towards wind-up and buyout is rapidly growing, and a material backlog may be building up!

Demand is outstripping supply

The increasing demand for bulk annuity transactions has driven a material increase in the resources needed from scheme and insurer administration functions. Capacity planning is now a key concern for DB pension risk transfer stakeholders.

Developments in legislation and regulation are demanding even more administration resource to complete essential projects such a GMP Equalisation, and preparing schemes for plugging in to the long-awaited Pensions Dashboard ecosystem.

The talent pool of experienced defined benefit pension administrators is limited. Third-party administrators and bulk annuity insurers are competing for the same candidates, while demand continues to increase. Solving this skills shortage requires investment in technology, people, and processes.

When a scheme enters into a full scheme buy-in, there is a contractual agreement in the bulk annuity policy whereby the Trustees are “contractually bound” to complete the post buy-in data and benefits cleansing within a defined period (normally no more than 18 to 24 months).

Completion of this work will enable the Trustees and insurer to “true-up” the bulk annuity policy to reflect the final cleansed data and benefits, rectifying any historical issues or errors identified, and then move to wind-up the scheme and have individual policies issued to members.

Failing to meet these contractual commitments can result in additional costs, risks, further resource requirements, delays and uncertainty for the insurer over the scheme’s progression and move to buyout.

Consequences of inaction

Not getting on top of data quality sooner rather than later exposes scheme to a multitude of consequences.

Poor data represents more risk to insurers. This will translate into the level of interest from insurers to transact, and the resulting pricing offers. Less interest creates a less competitive environment, less choice of insurers and potentially a sub-optimal pricing outcome.

Those insurers who do agree to quote, who fear the risk of poor data and benefits quality, will add their own margin for prudence and uncertainty to the pricing offered. Posing another threat to a pricing increase and drop in value offered.

More costs could be incurred post buy-in should additional data cleansing work or incomplete data projects such as GMP Equalisation be found. This can also cause delays to anticipated timelines creating further expense from ongoing operations while the data work is being completed. Money that might be requested from the Sponsor or deplete any available surplus which could have been used to enhance member’s pensions and/or refunded to the sponsor.

Any errors or issues in the current data and benefits will simply continue to grow, compounding in magnitude and scale over time. Sometimes these rectifications can prove extremely challenging. Not to mention the possible hardships suffered by the member for longer than necessary, not able to truly benefit from any rectification in their favour (due to being now very old or even having passed away).

Root causes – how did we get here?

The culture in pensions administration delivery has been one of lowest price wins. The pace of technological change has been much slower in the DB pensions world than any other area of financial services.

There has not, until now, been the capability to easily and affordably clean and fix scheme data. Even when the opportunity to tackle these issues has been presented, the cost of such projects has discouraged the trustees from opening that can of worms. Instead opting to ‘lift’ and ‘drop’ from one system to the other. Replicating issues and errors already in place.

This was partly driven by inefficient systems and processes for undertaking such exercises, often resulting in eye-watering fee proposals.

This is no longer the case.

In today’s marketplace, leading edge administration platforms can make this cost-effective and result in material efficiencies allowing administrators to focus on truly added value work and enable more self-service from scheme members.

At the same time, the volume of “project” work required of administration functions (both on the Trustee side and on the insurer side) is rapidly growing and expected to continue to do so. Resulting in third party administrators and bulk annuity insurers all implementing material investments in recruiting, training and systems development – unfortunately the lead time to deliver the outcomes from these investments is lagging behind the demand in the DB pension risk transfer marketplace.

What can be done?

Investing now to better understand the nature and quality of your data pays dividends downstream. This initial preparation is critical for a smooth DB pension risk transfer. It creates more certainty over the costs and liabilities of the pension scheme and improves the credibility of a pension scheme to the pension risk transfer marketplace.

If you have completed a buy-in, meeting your contractual commitments will be vital. Any delays in data and benefits cleansing will open your scheme up to uncertainties over costs and timings. We are even seeing schemes, post buy-in, looking at changing administration provider to unlock issues and conclude these commitments in a well-managed and cost-effective way.

For many schemes, the requirement to plug into the Pensions Dashboard will result in some data cleanse activity to enable connection in a robust way – why not extend this to a more thorough and complete exercise?

If you are peeking inside Pandora’s box, why not throw it open and upgrade your entire data and benefits quality? At the end of the day, this is aligned to meeting your contractual commitments as Trustees to your scheme members to pay the right benefits to the right members.

The advent of improved technology and platforms supports efficient and effective means of auditing and checking data. Scheme members are becoming ever more adept at using “member apps” and these can be used for data verification purposes, reducing the reliance on paper-based communications (and more importantly the creaking postal system). Then the better systems out there can automatically determine corrected benefit entitlements and kick off the rectification process to put the member into the position they should have been (along with back payments etc).

If you are peeking inside Pandora’s box, why not throw it open and upgrade your entire data and benefits quality?

Martyn Phillips

At the end of the day, this is aligned to meeting your contractual commitments as Trustees to your scheme members to pay the right benefits to the right members.

Get your house in order, why pension data quality can’t wait

Getting your data and benefits right now is an investment in the future. Even before embarking on a process to seek quotes for a bulk annuity, it will deliver material rewards to your scheme members. You wouldn’t buy a house without a survey (effectively an audit) and consequential corrections (indemnities, repairs etc), so why would you not do the same with your scheme data and benefits?

If you are thinking of changing administration provider, why not break that general “mould” and use that as the opportunity to identify and resolve any data and benefits issues?

If you aren’t able to embrace and deliver on improving the quality of your data and benefits, you could end up being left with multiple challenges:

- Insufficient insurer interest in a busy bulk annuity marketplace, reducing or removing your ability to potentially increase the long-term security of your members’ benefits

- Uncertainty of the long-term costs of operating the pension scheme

- Unexpected and unpleasant costs as and when any issues are finally uncovered

- Finding the waiting list has grown even more, delaying or deferring any strategic plans you or the scheme sponsor had for the pension scheme

Start the conversation, strengthen your scheme

Speak to your chosen administration provider now about what may be possible and when. Start building a strategy to enhance and improve the quality of the data and benefits and establish best in breed practices. Use the best available administration technology to ensure the greatest chance of maintaining the highest quality of data and benefits going forward.

And maybe, just maybe, spending a small part of the possible surplus that exists in your scheme to bring clarity, accuracy and efficiency to your data and benefits will create even greater certainty over what surplus may be left!