Funding

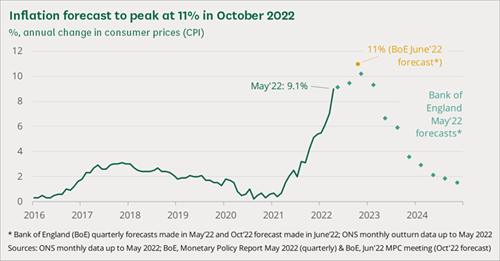

Funding defined benefit pensions is a long-term game. The Bank of England forecasts that high inflation will last around two years and will reduce to the long-term target of 2% p.a. after this. Trustees, therefore, should not make any knee jerk reactions.

Pension benefits are inflation linked, but in most cases subject to a cap. If inflation continues to rise, it is unlikely that liabilities will significantly increase as caps are biting.

Investment

Inflation linked assets will increase in value as inflation rises. If assets are hedging inflation risk, they will rise to match rises in liabilities. However hedging may get out of sync as caps are hit – trustees may need to revisit hedging strategies to ensure they remain appropriate.

Administration

Pension scheme members are likely to read about high inflation in the news and administrators may get more queries than normal. High inflation will erode the value of benefits.

Trustees may wish to consider discretionary increases where there is appetite/funds to do so. It is relatively common for schemes to contain a power to provide additional (discretionary) pension increases but employer consent is usually needed. Trustees may want to review their rules to check whether there is a discretionary increase provision. If there is, consideration can then be given to whether or not it should be exercised and, if so, to what extent. It would be sensible to document the trustee considerations, whether or not the discretionary increase power is used.

Administrators should be aware of anomalies that may exist to ensure that members are not disadvantaged by taking a certain course of action, given high inflation levels. For example, a deferred member giving up uncapped deferred revaluation for capped pension increases. Transfer values for members close to retirement may also need careful consideration. Trustees may want to consider a generic communication to members around issues to consider in light of high inflation.

Company Accounting

Accounting figures are normally carried out on a roll-forward basis, where liability figures are estimated rather than recalculated on a member by member basis.

It is important that this estimate allows correctly for inflation, as allowing for actual inflation over the year may exceed the employer’s materiality limits.